Prudence Concept in Accounting

Alternatively the NBFCs may also follow the concept of Trading Book as per the extant prescriptions for NBFCs. C Within each time bucket there could be mismatches depending on cash inflows and outflows.

What Is The Prudence Concept Youtube

The prudence principle of accounting also known as the conservatism principle states that a business should exercise a good degree of caution when booking incomes and expenses.

. Thus if you were to create a continuum with optimism on one. Eg the Prudence concept Prudence Concept Prudence Concept or Conservatism principle is a key accounting principle that makes sure that assets and income are not overstated and provision is made for all known expenses and losses whether the amount is known for certain or just an estimation ie. Such a control demand does not seem to be of minor importance at.

An accounting period is the interval of time during which accounting activities are measured. While the mismatches up to one year would be relevant since these provide early warning signals of impending liquidity problems the main. The concept of materiality in accounting is subjective relative to size and importance.

The items that have very little or no impact on a users decision are termed as immaterial or insignificant items. It is classically considered to be a virtue and in particular one of the four Cardinal virtues which are with the three theological virtues part of the seven virtues. Alongside this expenses should be booked as soon as a reasonable likelihood of.

This aspect of the materiality concept is more noticeable when comparing companies that vary in size ie a large company vis-à-vis a small company. Financial information might be of material importance to one company but stand immaterial to another company. Instead what you are striving for is to record transactions that reflect a realistic assessment of the probability of occurrence.

A state list or identify accounting concepts terms and principles. The materiality concept of accounting stats that all material items must be properly reported in financial statementsAn item is considered material if its inclusion or omission significantly impacts the decision of the users of financial statements. C demonstrate an understanding of basic accounting concepts conventions and principles.

The prudence concept does not quite go so far as to force you to record the absolute least favorable position perhaps that would be entitled the pessimism concept. Prudentia contracted from providentia meaning seeing ahead sagacity is the ability to govern and discipline oneself by the use of reason. A apply accounting concepts and principles to analyze issues.

This accounting concept promotes prudence in accounting. Ii Application The ability to. The four most important financial statements in accounting are.

In particular is considered wise to book an income only when it is realized. Summarizes financial results for an. Double -entry book keeping principles including the maintenance of accounting records a Identify and explain the function of the main data sources in an accounting systemK.

Expenses and liabilities are not understated in. Prudentia is an allegorical female personification of the. It means that for the purposes of accounting the business and its owners are to be treated as two separate entities.

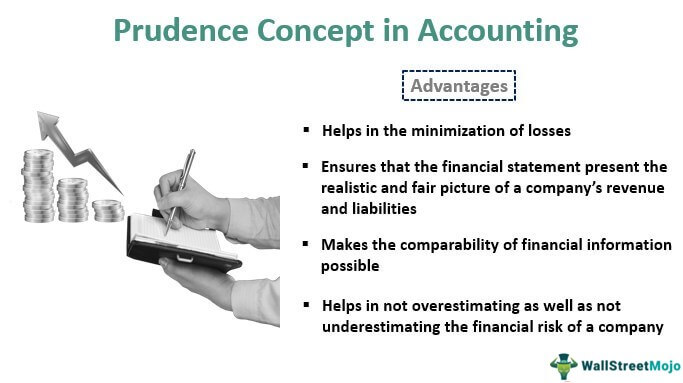

It states that profit should not be included until it is realized. Cameral accounting was developed as early as the 16th century onwards in order to contribute to increased control of public money. Prudence concept is a very fundamental concept of accounting that increases the trustworthiness of the figures that are reported in the financial statements of a business.

221 Business Entity Concept The concept of business entity assumes that business has a distinct and separate entity from its owners. The concept advises that the final accounts of a company must always show caution while reporting any figures specifically impacting the income and expenses. The concept of the accounting period is an important one for financial statements.

B define and explain accounting concepts principles theories and procedures. Common accounting periods include monthly quarterly and annually. So all losses are recognized those that have occurred or.

However losses even those not realized but with the remote possibility of occurring should be included in the financial statements. A similar cost may be. Keeping this in view.

Accounting conceptsK Materiality ii Substance over form iii Going concern v Accruals vi Prudence Consistency C The use of double-entry and accounting systems 1. It means that the preparer must.

Prudence Concept Ceopedia Management Online

Prudence Of Concept Why Is Prudence Important In Accounting

Prudence Financiopedia

Prudence Concept In Accounting Overview Guide

Comments

Post a Comment